Final 2026 Open Enrollment Report: Household Income (> 400% FPL)

Sun, 04/12/2026 - 4:05pm

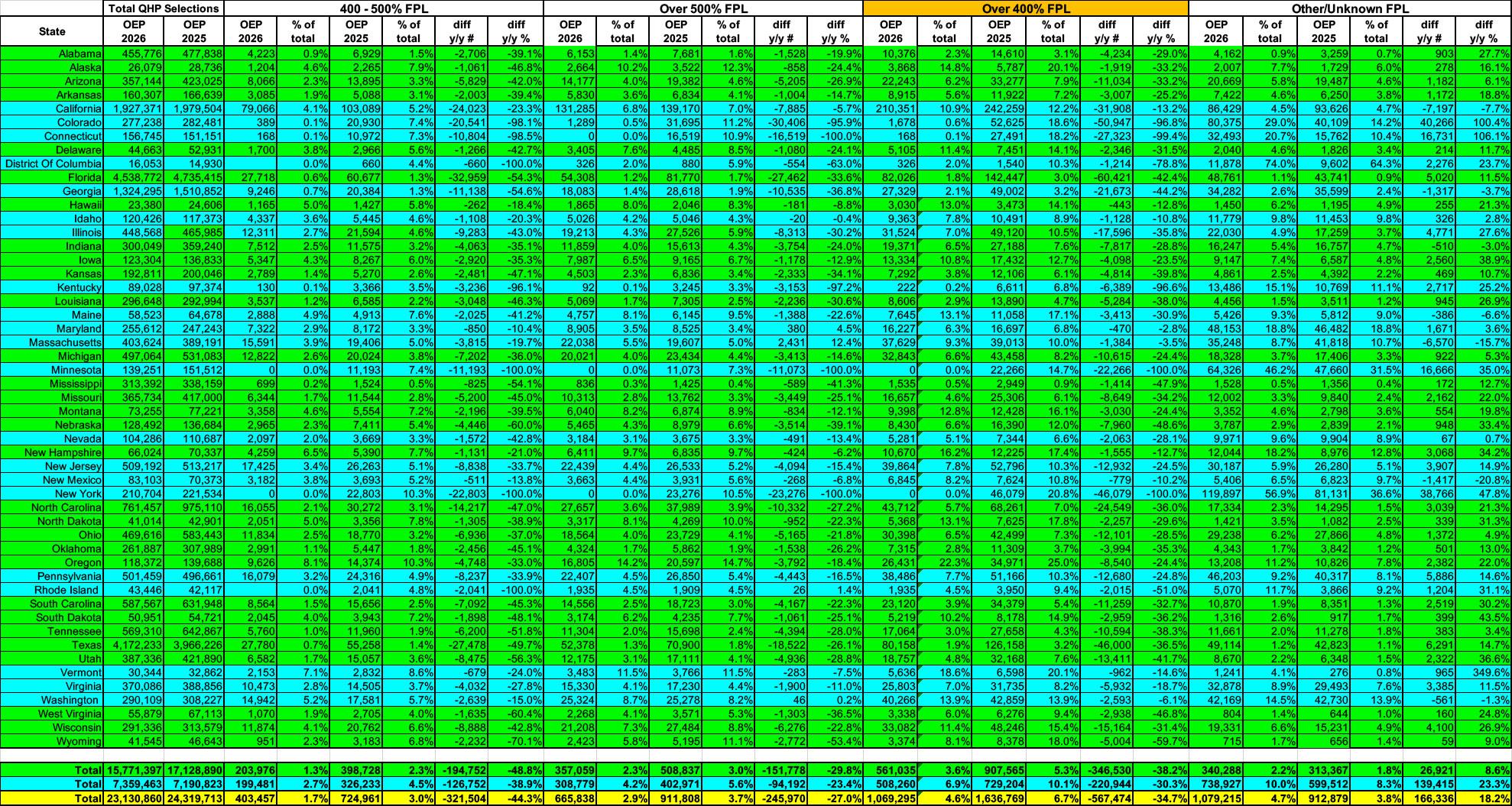

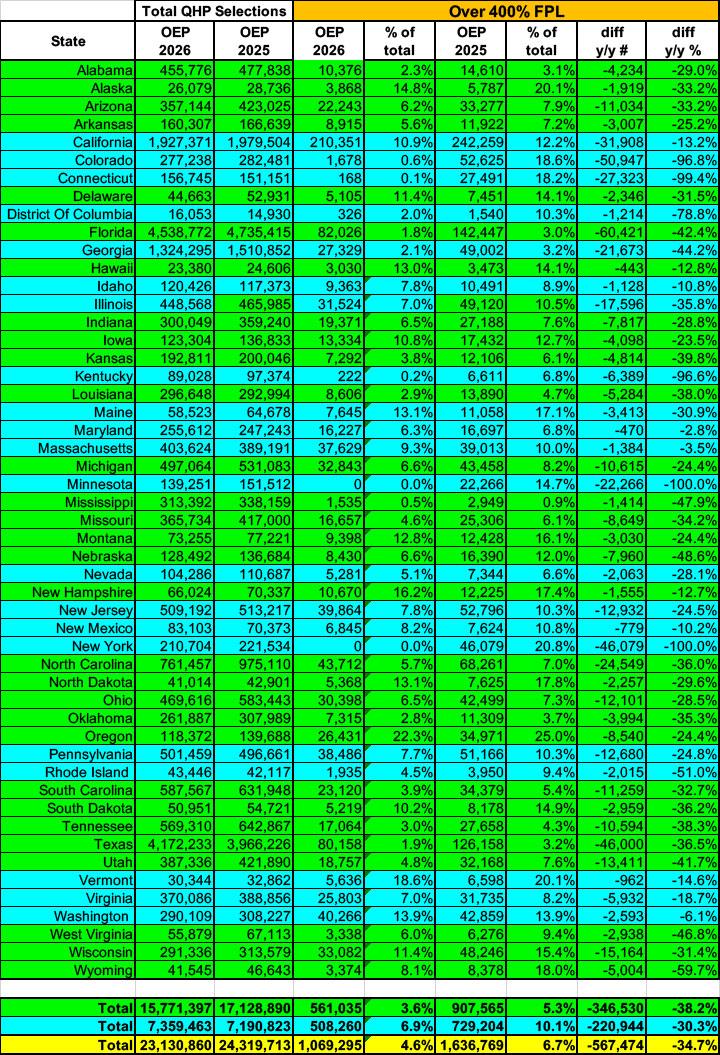

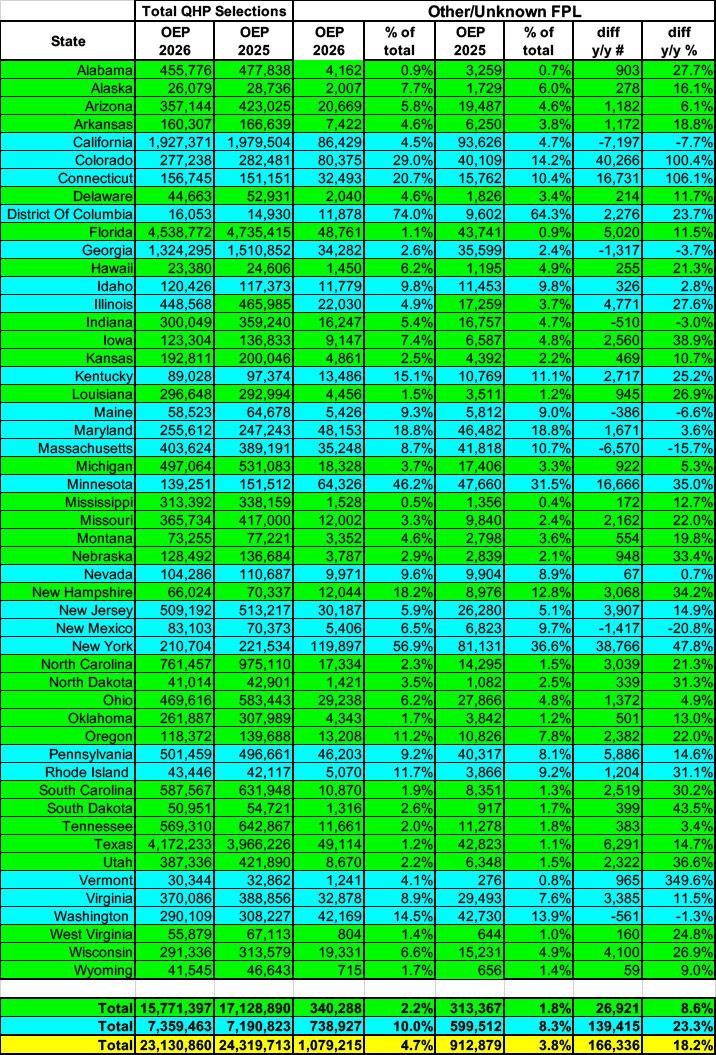

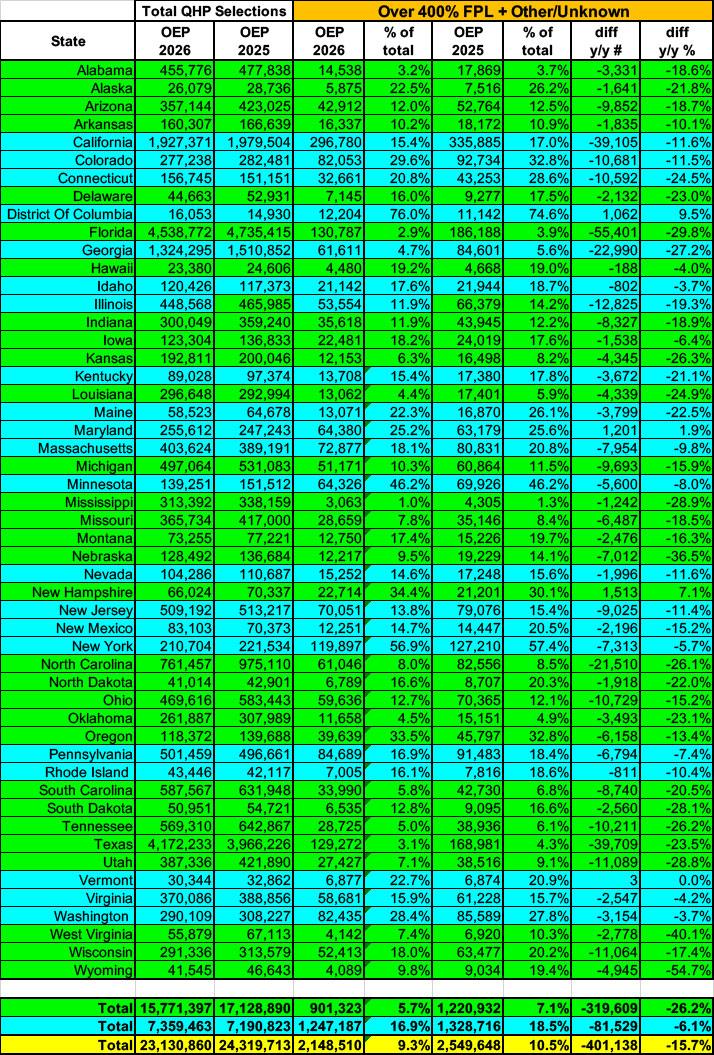

Finally, there's nearly 1.1 million exchange enrollees who earn more than 400% FPL...although this total is actually closer to 2.15 million if you include enrollees whose household income is either "other" or "unknown:"

Why is income data not available for all consumers?

The application only collects household income data when consumers are requesting financial assistance.

Consumers that do not request financial assistance do not enter their household income information and are classified as having an “Other/Unknown FPL.”

There are a few SBEs that classify consumers who enter their household income information but are determined not eligible for financial assistance as “Other/Unknown FPL”. As a result, some SBEs report zero plan selections in certain income categories. Please refer to the Public Use Files Definitions document for additional information on these data.

There are also a small number of consumers who requested financial assistance but may have missing incomes. For HealthCare.gov states, consumers may have missing incomes due to data anomalies or a tax filing status that makes them APTC-ineligible (e.g., married filing separately).

While enrollment from 400 - 500% FPL dropped by a stunning 44% (over 320,000 people), it's important to keep in mind that a significant number of enrollees who normally earn just over 400% FPL are likely taking steps (such as Health Savings Accounts and Individual Retirement Funds) to reduce their official MAGI income below that threshold in order to remain eligible for federal tax credits & avoid the dreaded "Subsidy Cliff."

I estimated that up to ~250,000 enrollees fall into this category; assuming that's fairly close, the actual drop in enrollment in the 400 - 500% FPL bracket could be as little as 70,000 or so, at least initially. Meanwhile, the "over 500% FPL" bracket saw a drop of around 245,000 plan selections, down 27% vs. last year.

Interestingly, the "Other/Unknown" bracket (which, again, mostly consists of people who failed to enter any household income projection whatsoever) actually increased by 18% year over year, from around 912,000 to 1.08 million people. While it's possible that a few enrollees who earn below 400% FPL failed to enter any income, I have to imagine that the vast majority of this crowd are households who know for certain that they aren't eligible for any financial help whatsoever and therefore earn more than 400% FPL (probably over 500% FPL in most cases).

Overall, enrollment over the 400% FPL threshold dropped by ~567,000 people (35%) if you only include the official definition, or by over 400,000 (over 15%) if you assume that every "Other/Unknown" enrollee also earns more than 400% FPL this year.

Again, assuming my estimates are fairly close, that means around 1/3 of this demographic are trying to squeeze in under the 400% threshold. Some will be successful…others won’t and will be hit with paying back every dime of subsidies that they’re receiving this year when they file their taxes a year from now.

It's also worth noting that there are now two states which don't have any exchange enrollees earning more than 400% FPL by the official definition (Minnesota & New York), plus several more where enrollment over 400% has dropped by more than 90% (Connecticut, Colorado & Kentucky).

There isn't a single state where it's increased (again, not including the "Other/Unknown" bracket)...the closest any state comes that is Maryland, where it still dropped by 2.8%.

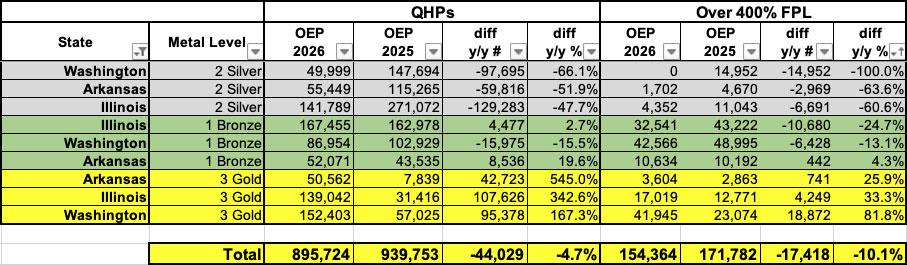

In terms of metal levels, there's not much to say here...over 400% FPL, Bronze enrollment dropped by 13%, Silver by 24% and Gold by 19% nationally. However, it is worth noting that across the 3 states which newly implemented premium alignment pricing this year, there was still a dramatic increase in Gold enrollment (and a correspondingly dramatic drop in Silver enrollment) even over the 400% threshold:

Advertisement