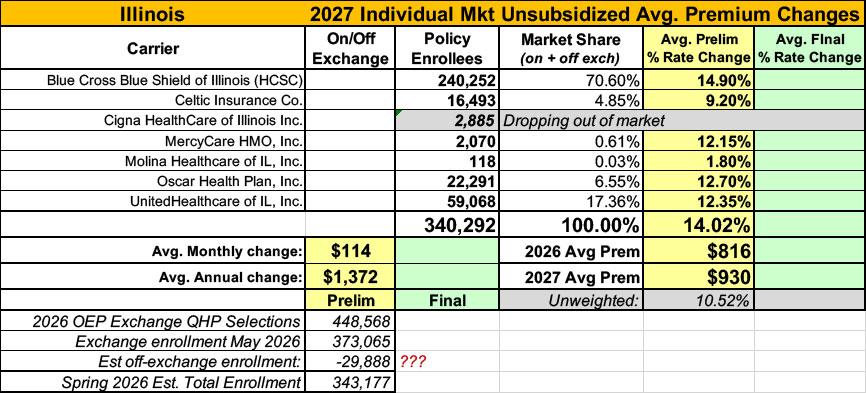

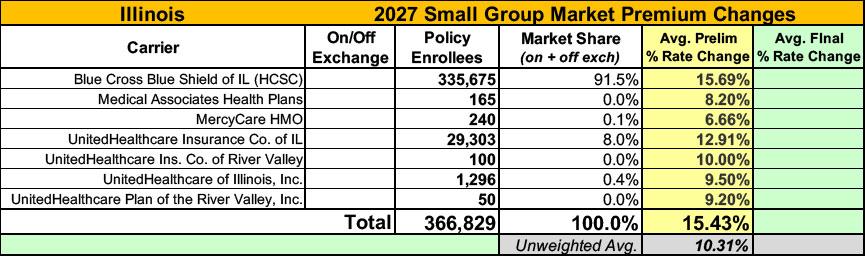

2027 Rate Changes - Illinois: +14.0% indy, +15.4% sm. group

Thu, 06/11/2026 - 2:28pm

via the Illinois Dept. of Insurance:

Affordable Care Act (ACA) - Illinois Rate Filings

The chart below contains proposed rates for Plan Year 2027, which will be reviewed for compliance with federal and state requirements. Please submit any comments to DOI.HealthRateReview@illinois.gov by Friday, July 10, 2026.

2026 Illinois On- and Off-Exchange Plan Analyses can be found here.

The Health Rate Review Consumer Guide can be found here.

How are rates developed?

Each year, health insurance companies determine future premiums based on a number of past factors.

These factors include, but are not limited to, hospital and prescription drug costs, enrollment figures, utilization trends, and inflation. Companies use these factors to project future consumer premium costs and ensure they can pay claims and remain financially stable. The ACA establishes an MLR which requires insurers to spend at least 80% of premiums collected in the individual and small group markets and requires insurers to spend at least 85% of premiums collected in the large group market.

Other factors that can impact consumer premium costs include age, location, the number of employees in an employer plan, and the type of plan a consumer chooses.

Under the ACA, a health insurance company may not use a consumer’s pre-existing conditions to deny coverage or determine a consumer’s premium rates.

What is the rate review process?

All individual and small group insurers are required to submit their rates to the Department annually by a deadline set by the Director of Insurance. Deadlines may change from year-to-year. After the rates are submitted, the Department is required to post the rates on its website within five (5) business days and then accept public comments for a period of 30 days. The Department must post all public comments within five (5) business days after the comment period ends.

The Director must then issue a decision approve, disapprove, or modify an insurer’s rates within 60 days. The Director must take public comments into account. If the Director does not issue a decision, the plan rates are automatically approved. The Department is required to notify the insurer of its decision and post the final rates on its website.

The Department uses credentialed actuaries and experts to determine whether rates are reasonable and adequate.

Where do I find the rate tables?

Individual and small group rates filed with the Department can be found here: Rate Filings. The Department posts an insurer’s initial average, maximum and minimum plan rate increases or decreases on the left-hand side of the table, and the Department posts an insurer’s final average, maximum and minimum plan rate increases or decreases on the right-hand side of the table. Links to the carrier’s rate filing or filings and the Department’s final decisions are posted on the far-right side of the table.

The initial rates filed by an insurer may vary from the final rates. The initial rates may also remain the same. After an insurer files their initial rates, the Director will determine whether the insurer’s rates are reasonable or adequate. If the insurer’s rates are found to be unreasonable or inadequate, the Director will adjust the final rates. If the insurer’s rates are found to be both reasonable and adequate, the Director will approve the rates without making any changes.

Oscar Health Plan:

The significant factors driving the proposed rate change include the following:

Medical & Prescription Drug Inflation & Utiliziation Trends

The projected premium rates reflect the most recent emerging experience which was trended for anticipated changes due to medical and prescription drug inflation and utilization.

Administrative Expenses, Taxes & Fees, and Risk Margin

Changes to the overall premium level are needed because of required changes in federal and state taxes and fees. In addition, there are anticipated changes in both administrative expenses and targeted risk margin.

Prospective Benefit Changes

Plan benefits have been revised as a result of changes in the Center for Medicare and Medicaid Services (CMS) Actuarial Value Calculator and state requirements, as well as for strategic product considerations.

Anticipated Changes in the Average Morbidity of the Covered Population

Changes to the overall premium level are needed because of anticipated changes in the underlying morbidity of the projected marketplace.

UnitedHealthcare of Illinois:

Some of the key healthcare cost trends that have affected this year’s rate actions include:

- Increasing cost of medical services: Annual increases in reimbursement rates to healthcare providers, such as hospitals, doctors, and pharmaceutical companies.

- Increased utilization: The number of office visits and other services continues to grow. In addition, total healthcare spending will vary by the intensity of care and use of different types of health services. The price of care can be affected using expensive procedures such as surgery versus simply monitoring or providing medications.

- Higher costs from deductible leveraging: Healthcare costs continue to rise every year. If deductibles and copayments remain the same, a higher percentage of healthcare costs need to be covered by health insurance premiums each year.

- Impact of new technology: Improvements to medical technology and clinical practice often result in the use of more expensive services, leading to increased healthcare spending and utilization.

- Changes in market morbidity: Premiums reflect a modest increase in expected claims costs due to federal changes to premium subsidy eligibility for certain immigrant populations in 2027. These changes are expected to lead to some healthier members exiting coverage, resulting in a slightly higher average risk level and a small upward impact on premiums.

MercyCare HMO: (unfortunately, most of their actuarial memo is redacted)

Rate changes reflect changes in medical and pharmacy benefit cost, both price changes and changes in utilization. They also reflect the cost of CMS risk adjustment transfer payments borne by the plan, along with changes in administrative expenses.

Celtic Insurance Co: (again, much of the memo is redacted)

Impact of eAPTC Expiration

To account for eAPTC expiration prior to the 2027 benefit year, we have assumed rates will increase due to anticipated reductions in enrollment, both at the issuer and single risk pool level. As eAPTCs expire and enrollees subsequently face increased out-of-pocket premiums, we assume healthier individuals who tend to be more price sensitive will leave the market, worsening the average morbidity of the individual risk pool.

Health Care Service Corporation (BCBS IL): Welp.

It's also worth noting that Cigna, which is dropping out of the ACA market entirely, has around 2,900 effectuated enrollees in Illinois who will have to find other coverage this fall for 2027.

Letter of Intent to Discontinue Participation in the Illinois Individual Medical Market

Dear Ann Gillespie:

Cigna Healthcare (“Cigna”) submits this letter to formally notify the Illinois Department of Insurance (the “Department”) of its intent to discontinue participation in the Illinois Individual Medical Market, effective January 1, 2027.

This notice is provided pursuant to 50 Ill. Adm. Code § 2025.70 (Discontinuance of a Market) and 50 Ill. Adm. Code § 2025.40 (Notice Requirements), as well as applicable federal requirements governing guaranteed renewability and market withdrawals under 45 CFR §§ 146.152, 147.106, and 148.122.

After careful consideration, Cigna has determined that continued participation in the Illinois Individual Medical Market is not viable over the long term due to scale limitations and the operational demands of competing in a highly dynamic regulatory and market environment. This decision applies only to Individual Medical products and does not affect Cigna’s Individual Market dental offerings, which will continue without interruption.

The details of our Individual medical market exit include the following:

- Number of Lives Impacted: 2,885 (including both on and off exchange)

- Affected Illinois Counties: Cook, DuPage, Grundy, Kane, Kankakee, Kendall, Lake, McHenry and Will

- Product Forms Impacted: On Exchange CCGH-134525701 and Off Exchange CCGH-134602242

- Effective Date of Non-renewal: January 1, 2027.

- Line of Business Impacted: Individual HMO

In any event, this works out to a 14% average requested rate hike for the Illinois individual market next year, and a 15.4% average increase for small group enrollees.

It's also worth noting that the Illinois ACA exchange individual market as of March 2026 is a whopping 17% lower than the number who selected policies during Open Enrollment, which I'll discuss in more detail in a separate blog post soon...

Advertisement